Long-term disability insurance is one of those topics many people know little about—until they need it. Life can take unexpected turns. An injury or illness could make you unable to work for months, years, or even longer. In these moments, your regular income may stop, but your bills do not. Long-term disability insurance helps fill this gap, providing financial support when you are unable to work due to a serious health problem.

Many people believe that government or employer benefits will be enough. Unfortunately, these options often fall short, leaving families under stress. This article explains what long-term disability insurance is, who needs it, how it works, and how to choose a good plan.

You’ll also see examples, comparisons, and answers to common questions, all in clear, simple English.

What Is Long-term Disability Insurance?

Long-term disability (LTD) insurance pays a part of your income if you cannot work because of a long-term medical condition. The idea is to replace a portion of your paycheck, so you can cover living expenses—like rent, food, and healthcare—while you recover.

How does it work? If you become disabled, you first wait out a period called the elimination period (usually 90–180 days). After that, the insurance starts paying you a monthly benefit. Payments continue until you recover, reach the end of the benefit period, or hit the policy’s maximum age (often 65).

Why Is Long-term Disability Insurance Important?

Most people rely on their income to support themselves and their families. Losing this income—even for a few months—can create serious financial problems.

Here are important facts to consider:

- 1 in 4 workers will face a disability lasting more than 90 days before age 65 (U.S. Social Security Administration).

- Most disabilities are caused by illnesses, not accidents.

- Savings alone are often not enough. The average disability claim lasts nearly three years.

Employer-provided disability coverage is often limited. It may cover only a portion of your salary, or have strict rules about what counts as “disabled.” Government programs like Social Security Disability Insurance (SSDI) can be hard to qualify for and pay only modest amounts.

Who Needs Long-term Disability Insurance?

Some people think only those with dangerous jobs need this insurance. The truth is, most long-term disabilities are due to illnesses like cancer, heart disease, or back problems—not workplace accidents.

You should consider long-term disability insurance if you:

- Rely on your income to pay for living expenses

- Have family members who depend on you financially

- Are self-employed or do not have strong employer benefits

- Want to protect your savings and retirement plans

Even if you have employer coverage, check the details. Many group plans are not enough for most families.

Key Features Of Long-term Disability Plans

Long-term disability insurance policies can be complex. Understanding the main features helps you choose wisely.

1. Benefit Amount

This is the monthly payment you receive if you become disabled. Most plans cover 50%–70% of your pre-disability income.

2. Benefit Period

This is how long you can receive payments. Common options:

- 2 years

- 5 years

- Until age 65

Longer benefit periods cost more, but give more security.

3. Elimination Period

This is the waiting time before benefits begin, usually 90–180 days. Choosing a longer elimination period lowers your premium, but means you need more savings to cover the gap.

4. Definition Of Disability

Policies define “disability” in different ways. The two main types:

- Own Occupation: You are considered disabled if you can’t do your own job.

- Any Occupation: You are considered disabled only if you can’t do any job you are qualified for.

“Own occupation” is more generous, but costs more.

5. Non-cancellable And Guaranteed Renewable

A non-cancellable policy means the insurer cannot raise your rates or cancel your coverage, as long as you pay premiums. Guaranteed renewable means your policy will be renewed, but the insurer can raise rates for everyone in your group.

6. Optional Riders

You can add extra benefits to your policy, called riders. Common options include:

- Cost-of-living adjustment (COLA): Increases your benefits over time to keep up with inflation.

- Future increase option: Lets you buy more coverage later, if your income rises.

- Partial disability benefit: Pays a part of your benefit if you can work part-time.

Credit: www.hauptman-obrien.net

How Much Does Long-term Disability Insurance Cost?

Premiums depend on many factors, including your age, health, job, income, and the policy features you choose.

On average, you can expect to pay 1%–3% of your annual income for a private long-term disability policy. For example, if you earn $60,000 per year, your annual premium might be $600–$1,800.

Below is an example comparison for a healthy 35-year-old non-smoker earning $60,000 per year:

| Feature | Plan A (Basic) | Plan B (Comprehensive) |

|---|---|---|

| Monthly Benefit | $3,000 | $4,000 |

| Benefit Period | 5 years | To age 65 |

| Elimination Period | 90 days | 180 days |

| Own Occupation | No | Yes |

| Monthly Premium | $75 | $120 |

Employer Vs. Individual Plans

You can get long-term disability insurance through your employer or buy your own individual policy. Each option has pros and cons.

| Feature | Employer Plan | Individual Plan |

|---|---|---|

| Cost | Usually lower or free | You pay the full premium |

| Coverage | Basic, limited options | Customizable, higher limits |

| Portability | Lost if you leave your job | Stays with you |

| Taxation | Benefits usually taxed | Benefits usually tax-free |

| Underwriting | Minimal health checks | Full health review |

A common mistake is to rely only on an employer plan. If you change jobs or lose your job, you may lose your coverage. Individual plans are more flexible and portable.

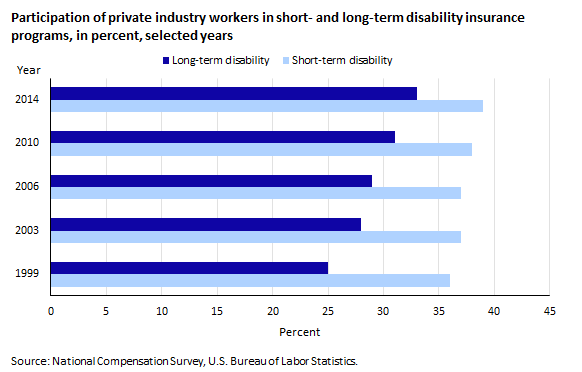

Credit: www.bls.gov

How To Choose The Right Long-term Disability Plan

Buying disability insurance is not only about the price. It’s about getting real protection when you need it. Here are steps to help you choose:

1. Calculate How Much Income You Need

Look at your monthly expenses: rent/mortgage, food, utilities, insurance, and any debt payments. Decide what you really need to cover if you can’t work.

2. Review Existing Coverage

Check if you have any coverage from your employer or government. See if it’s enough, and what the rules are.

3. Compare Policies

Get quotes from different insurance companies. Pay attention to:

- Definition of disability

- Benefit amount and period

- Exclusions (what is not covered)

- Premiums and possible rate increases

4. Consider Optional Riders

Think about adding riders for inflation protection, future income growth, or partial disability.

5. Check Insurer Reputation

Choose a company with strong financial ratings and good customer service. Claims should be paid fairly and on time.

Non-obvious insight: Some people buy only the cheapest policy, but this can be a mistake. A plan with a strict “any occupation” definition may not pay if you are unable to do your job, but can do another lower-paying job. Look for policies that fit your actual occupation and income level.

Common Exclusions And Limitations

Not every disability is covered. Most policies do not cover:

- Disabilities caused by self-inflicted injuries

- Disabilities from war or criminal acts

- Pre-existing conditions (illnesses you had before buying the policy, for a set period)

- Short-term conditions (usually anything lasting less than the elimination period)

Mental health conditions and substance abuse may have shorter benefit periods or lower maximums.

Credit: n-hlaw.com

How To File A Claim

If you become disabled, here’s what you should do:

- See your doctor and get medical records to prove your condition.

- Notify your insurer as soon as possible.

- Complete claim forms (employer and/or physician statements may be required).

- Cooperate with the claims examiner. They may ask for more medical evidence or updates.

- Follow treatment plans. Not following medical advice can lead to denial.

A non-obvious tip: Keep a detailed diary of your symptoms and treatments. This can help support your claim if questions arise.

Real-world Example

Consider Maria, age 40, a project manager earning $80,000 per year. She developed a chronic illness and could not work for two years. With an LTD policy replacing 60% of her income, she received $4,000/month. This helped her pay her mortgage, cover living expenses, and avoid using up her retirement savings.

Without the policy, her family would have faced serious financial trouble.

Important Statistics

- Nearly 5.6% of working Americans experience a short-term disability each year.

- Only 40% of U.S. adults have enough savings to cover a $1,000 emergency.

- More than 90% of long-term disabilities are caused by illnesses, not accidents.

You can find more data from the Social Security Administration.

How Long-term Disability Differs From Other Coverage

You may hear about other types of disability and income protection. Here’s a quick summary:

| Type | Main Feature | Typical Benefit Period |

|---|---|---|

| Short-Term Disability | Replaces income for temporary conditions | Up to 6 months |

| Long-Term Disability | Covers serious, lasting disabilities | 2 years to age 65 |

| Workers’ Compensation | Covers work-related injuries/illnesses only | Varies (may be short or long term) |

| Social Security Disability | Strict rules, pays only for total disability | Until retirement age |

Long-term disability insurance is the only option designed to cover most illnesses and injuries—whether they happen at work or not.

Frequently Asked Questions

What Is The Elimination Period In Long-term Disability Insurance?

The elimination period is the waiting time after you become disabled before your benefits begin. Common periods are 90, 120, or 180 days. You must be disabled the entire time before payments start.

Is Long-term Disability Insurance Worth It If I Am Young And Healthy?

Yes. Premiums are lower when you are young and healthy. Disabilities often happen because of illness, not just age or accidents. Buying early locks in lower rates and protects you before problems arise.

Will My Long-term Disability Benefits Be Taxed?

If your employer pays the premium, benefits are usually taxable. If you pay for your own policy with after-tax money, benefits are tax-free. Check with your insurer and a tax advisor.

Does Long-term Disability Insurance Cover Mental Health Conditions?

Some policies cover mental health conditions, but benefits may be limited to 12–24 months. Always check your policy’s details for specific rules.

Can I Buy Long-term Disability Insurance If I Am Self-employed?

Yes. In fact, it’s especially important for self-employed people, since you don’t have employer coverage. You can buy an individual policy to protect your income.

Getting the right long-term disability insurance plan means taking time to understand your needs, comparing options, and not just choosing the cheapest policy. When you protect your income, you also protect your future and your family’s well-being.

Read More:

- Critical Illness Insurance Plans: Protect Your Future Today

- Professional Indemnity Insurance Coverage: Essential Protection Tips

- Cheapest Sr22 Insurance Providers: Top Picks for Budget Drivers

- Landlord Insurance for Rental Properties: Essential Coverage Guide

- Best Life Insurance for Diabetics: Top Plans and Savings Tips

- Best Insurance CRM Software 2026: Top Solutions for Agencies

- Boat Insurance Coverage Options: What You Need to Know

- Car Insurance for Teen Drivers: Save Money and Stay Protected