Owning rental property can be a smart way to build wealth. But with that opportunity comes risk. Fires, storms, lawsuits, and even bad tenants can all lead to big losses. That’s why many property owners choose landlord insurance. If you’re renting out a house, apartment, or even just a room, understanding landlord insurance is vital. This guide will walk you through everything you need to know, using simple language and practical examples.

What Is Landlord Insurance?

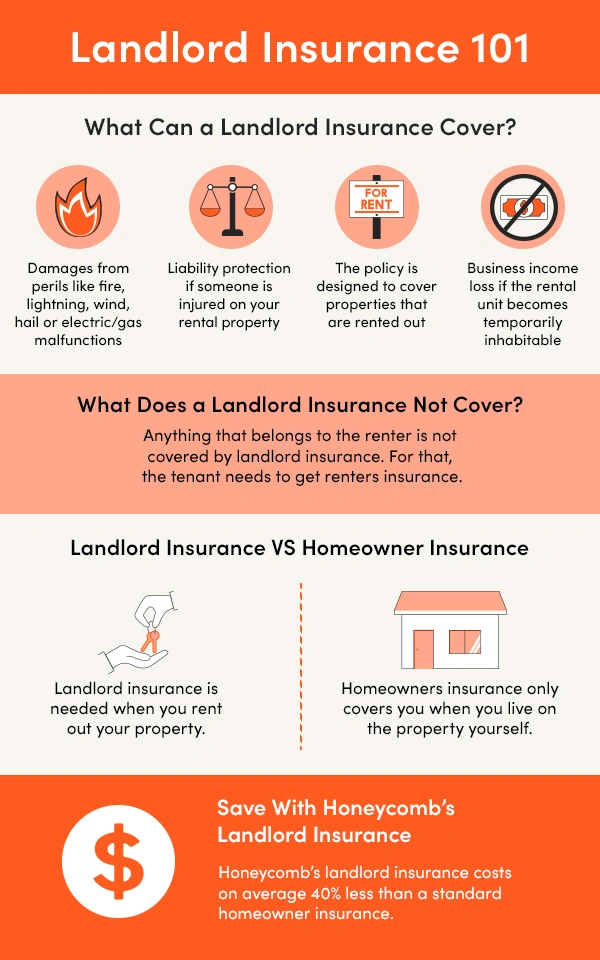

Landlord insurance is a special type of insurance policy for people who rent out their property. It protects owners from financial losses caused by damage, accidents, or legal claims linked to their rental. Unlike regular homeowners insurance, landlord insurance is designed specifically for rental risks.

For example, if a tenant accidentally starts a kitchen fire, landlord insurance may help pay for repairs. Or if someone gets hurt on the property and sues you, the policy can cover legal fees and damages. In short, landlord insurance helps keep your investment safe from unexpected events.

Why Landlord Insurance Matters

Many new landlords believe their regular homeowners policy is enough. This is a common mistake. Most homeowners insurance does not cover damages or liability from renting. If you rent your home—even for a short time—you may have no coverage at all without a landlord policy.

Here’s why landlord insurance is important:

- Protects your property from risks like fire, storms, or vandalism

- Covers lost rental income if the property becomes unlivable after a covered loss

- Provides liability protection if someone is injured and blames you

Without the right policy, you may have to pay out of pocket for repairs or lawsuits. That can turn a profitable rental into a financial disaster.

Credit: www.nationaldoorsteppickup.com

What Does Landlord Insurance Cover?

Most landlord insurance policies include three main types of protection. However, coverage can vary between insurance companies, so always read the policy details.

1. Property Damage

This covers physical damage to your building caused by things like:

- Fire

- Wind and hail

- Lightning

- Vandalism

- Burglary

Example: A storm blows a tree onto your rental home, damaging the roof. Your policy helps pay for repairs.

2. Liability Protection

If someone is injured on your property and claims you’re responsible, landlord insurance can help pay for:

- Medical costs

- Legal fees

- Court judgments

Example: A tenant’s guest slips on icy stairs and breaks a leg. They sue you for hospital bills. Liability coverage steps in.

3. Loss Of Rental Income

If your property is damaged by a covered event and becomes uninhabitable, this part of your policy can reimburse you for lost rent while repairs are made.

Example: A kitchen fire means your tenant must move out for two months. You can’t collect rent during this time, but your insurance covers the lost income.

Optional Add-ons

Landlord insurance can often be customized. Common optional add-ons include:

- Flood insurance (standard policies usually exclude flood damage)

- Earthquake insurance

- Rent guarantee (protects against tenant nonpayment)

- Emergency breakdown cover (for systems like heating or plumbing)

What Landlord Insurance Does Not Cover

No insurance policy covers every possible risk. Here are some common things landlord insurance usually does not cover:

- Tenant’s personal belongings (tenants need their own renters insurance)

- Normal wear and tear (old carpet, faded paint)

- Maintenance issues (broken appliances from age)

- Pest infestations (bed bugs, rodents)

Knowing these limits helps you avoid surprises and keeps your property in good shape.

Landlord Insurance Vs. Homeowners Insurance

Many landlords wonder how landlord insurance compares to regular homeowners insurance. The table below highlights the main differences:

| Feature | Landlord Insurance | Homeowners Insurance |

|---|---|---|

| Property Damage | Yes (rental property only) | Yes (owner-occupied only) |

| Liability Coverage | Yes (for tenant injuries/claims) | Yes (for owner/family injuries/claims) |

| Lost Rental Income | Yes | No |

| Tenant’s Belongings | No | Yes (if owner lives there) |

| Price | Usually higher | Usually lower |

In short, landlord insurance is tailored for rental situations, while homeowners insurance is for owner-occupied homes.

Key Factors When Choosing Landlord Insurance

Selecting the right policy can feel overwhelming. Here are the most important points to consider:

1. Property Type

Is it a single-family home, condo, or apartment building? Coverage needs can differ.

2. Location Risks

Properties in flood zones, wildfire areas, or cities with high crime may need extra coverage.

3. Tenant Type

Student housing, short-term rentals (like Airbnb), or long-term tenants each have unique risks.

4. Coverage Limits

Make sure your policy covers the full replacement cost of the building, not just the mortgage amount.

5. Deductible

Higher deductibles lower your premium but increase your cost if you file a claim.

6. Optional Coverages

Decide if you need extras like rent guarantee or emergency breakdown coverage.

7. Insurer Reputation

Choose companies with good customer service and fast claims processing.

How Much Does Landlord Insurance Cost?

The price of landlord insurance depends on several factors. On average, US landlords pay between $1,200 and $2,000 per year for a typical single-family rental property. This is usually about 20–30% higher than standard homeowners insurance.

Here are some factors that affect your cost:

- Property value and size

- Location (city, neighborhood)

- Age and condition of the building

- Security features (alarms, locks)

- Number of units

- Type of tenants (short-term vs. long-term)

Below is an example of how costs can vary by property type:

| Property Type | Average Annual Premium |

|---|---|

| Single-family home | $1,400 |

| Duplex | $1,900 |

| Small apartment (4 units) | $2,700 |

| Condo unit | $1,100 |

Tip: Bundling landlord insurance with other policies (like auto or umbrella coverage) can sometimes lower your total costs.

Common Mistakes Landlords Make

Many landlords, especially beginners, make costly errors when choosing or managing their insurance:

1. Not Updating The Insurer About Renting

If you don’t tell your insurer that you’re renting out your home, claims may be denied.

2. Underestimating Replacement Cost

Insuring for the mortgage balance, not the rebuild cost, can leave you short if disaster strikes.

3. Skipping Liability Coverage

Lawsuits can be expensive. Skipping this coverage is risky.

4. Ignoring Exclusions

Not reading the fine print means you may be surprised when something isn’t covered.

5. Not Requiring Renters Insurance

If tenants don’t have their own insurance, you may get drawn into costly disputes over lost or damaged belongings.

6. Choosing The Cheapest Policy Only

Lower premiums sometimes mean less coverage or slow claims service.

Real-world Example

Imagine you own a small duplex. One night, a pipe bursts in the upstairs bathroom and floods both units. The tenants must move out while repairs are made. Here’s how landlord insurance can help:

- Property damage: Repairs to walls, floors, and plumbing are covered.

- Loss of rental income: Your policy replaces the rent you lose while the home is being fixed.

- Liability protection: If a tenant claims you ignored the leaking pipe, your legal costs may be covered.

Without insurance, you’d pay for repairs, lost rent, and legal fees yourself.

How To Get The Best Deal

Getting the right landlord insurance isn’t just about price. Here’s how to find good value and protection:

- Compare quotes from at least three insurers. Coverage and costs can vary widely.

- Ask about discounts for things like smoke alarms, gated access, or bundling with other policies.

- Review your coverage yearly as property values and rental markets change.

- Work with an independent agent who understands rental properties.

A little research can save you money and headaches later.

Claims: How The Process Works

If something goes wrong, here’s how the claims process usually works:

- Contact your insurer as soon as possible after the incident.

- Document the damage with photos, videos, and a written description.

- Provide proof of ownership and value (receipts, appraisals).

- Meet with an adjuster sent by the insurance company.

- Repairs and payments are arranged according to your policy terms.

Tip: Keep records of all repairs and communications with tenants to speed up the process.

Landlord Insurance For Short-term Rentals

Renting on platforms like Airbnb or VRBO is popular, but it comes with unique risks. Standard landlord insurance may not cover short-term rental activities. Some insurers offer special policies for vacation rentals or homeshare properties.

Important points for short-term rentals:

- Tell your insurer how you’ll use the property

- Consider higher liability limits (more guests, more risk)

- Look for coverage against theft or guest-caused damage

Short-term renting without the right insurance can leave you exposed to big losses.

Credit: honeycombinsurance.com

Comparing Landlord Insurance Providers

Every insurer is different. Here’s a simple comparison of three well-known US providers:

| Company | Strengths | Weaknesses |

|---|---|---|

| State Farm | Strong reputation, wide coverage options | Premiums can be higher |

| Allstate | Good bundling discounts, easy online tools | Mixed customer service reviews |

| Liberty Mutual | Flexible add-ons, good claims process | Some limits on older buildings |

Always check reviews and ratings on trusted sites like the National Association of Insurance Commissioners or NerdWallet for more information.

Frequently Asked Questions

What Is The Difference Between Landlord Insurance And Renters Insurance?

Landlord insurance protects the property owner’s building, liability, and rental income. Renters insurance protects the tenant’s personal belongings and provides their liability coverage. Both are important, but they cover different things.

Is Landlord Insurance Required By Law?

No state or federal law requires landlord insurance, but most mortgage lenders do. Even if you own the property outright, it’s risky to go without coverage.

Does Landlord Insurance Cover Tenant Damage?

Most policies cover accidental damage caused by tenants (like a fire), but not intentional acts (like vandalism by a tenant). Always check your policy details.

Can I Get Landlord Insurance If I Only Rent Out One Room?

Yes. Many insurers offer policies for owners who rent a single room or a portion of their home. Be sure to tell your insurer exactly how you use the property.

How Can I Lower My Landlord Insurance Costs?

Increase your deductible, install safety features (smoke alarms, security cameras), and bundle with other insurance products. Comparing quotes is also a smart way to save.

Owning rental property can be rewarding, but it also means taking on risk. Landlord insurance is one of the best ways to protect your investment and your peace of mind. With the right policy, you can handle life’s surprises and focus on growing your rental business. Make informed choices, keep your coverage up to date, and you’ll be well prepared for whatever comes your way.

Credit: www.blockadvisors.com

Read More:

- Critical Illness Insurance Plans: Protect Your Future Today

- Long-Term Disability Insurance Plans: Protect Your Income for Life

- Professional Indemnity Insurance Coverage: Essential Protection Tips

- Cheapest Sr22 Insurance Providers: Top Picks for Budget Drivers

- Best Life Insurance for Diabetics: Top Plans and Savings Tips

- Best Insurance CRM Software 2026: Top Solutions for Agencies

- Boat Insurance Coverage Options: What You Need to Know

- Car Insurance for Teen Drivers: Save Money and Stay Protected