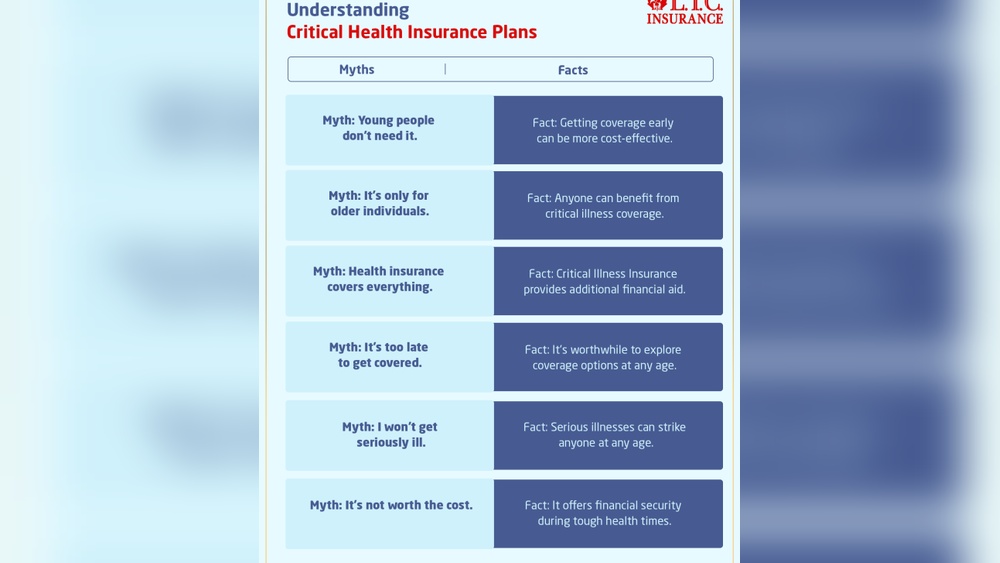

Many people think health insurance will cover everything if they become seriously ill. But in reality, major diseases like cancer, heart attack, or stroke often bring more than just hospital bills—they can mean lost income, expensive treatments, and major lifestyle changes. This is where critical illness insurance plans come in. They offer a lump-sum payment if you are diagnosed with a covered serious illness, helping you manage both medical and everyday costs during a tough time.

What Is Critical Illness Insurance?

Critical illness insurance is a special policy that pays you a fixed amount if you are diagnosed with a covered critical illness. Unlike regular health insurance, which pays hospitals or doctors directly for treatment, critical illness plans give you money to use however you need. This means you can cover out-of-pocket medical bills, pay your rent or mortgage, buy medicine, or even fund travel for specialized treatment.

For example, if someone with critical illness insurance is diagnosed with cancer, they can use the payout to cover expensive drugs, replace lost income, or pay for caregivers. There are usually a list of diseases the policy covers—like heart attack, stroke, cancer, kidney failure, and sometimes more.

Why Consider Critical Illness Insurance?

Serious illnesses can strike anyone, no matter their age or lifestyle. Medical costs are rising everywhere, but the real challenge is the hidden costs:

- Lost income if you are too sick to work for months or years

- Long-term care needs not covered by standard insurance

- Travel and accommodation costs for specialized treatment

- Daily living expenses while recovering

A 2022 study in the US found that over 60% of personal bankruptcies were linked to medical issues, even among those with health insurance. Many policies have high deductibles, co-pays, and limits. Critical illness insurance offers a financial cushion, so you can focus on recovery, not money worries.

How Does Critical Illness Insurance Work?

The process is simple:

- Choose a policy and coverage amount (for example, $50,000 or $100,000).

- Pay regular premiums (monthly, quarterly, or yearly).

- If you are diagnosed with a listed critical illness, you or your family files a claim.

- After verifying the claim, the insurer pays out the lump sum.

- You decide how to use the money.

Coverage usually starts after a short waiting period (often 30 days). If you survive a set number of days (often 14-30) after diagnosis, the benefit is paid. If you recover, you can use the money as you wish. If you pass away, some plans may pay your family, but most do not.

What Does Critical Illness Insurance Cover?

Every insurer has their own list of covered illnesses. Usually, the most common are:

- Cancer

- Heart attack

- Stroke

- Kidney failure

- Major organ transplant

- Coronary artery bypass surgery

Some plans may also cover paralysis, multiple sclerosis, blindness, or deafness. It’s important to check what is included and excluded in the policy. For example, not all types of cancer may be covered, and early-stage cancers are often excluded.

Here’s a simple comparison of what typical plans may cover:

| Illness | Basic Plan | Comprehensive Plan |

|---|---|---|

| Cancer | Yes | Yes (all stages) |

| Heart Attack | Yes | Yes |

| Stroke | Yes | Yes |

| Kidney Failure | Yes | Yes |

| Multiple Sclerosis | No | Yes |

| Early-Stage Diseases | No | Sometimes |

Credit: primeinvestor.in

Who Should Consider Critical Illness Insurance?

Critical illness insurance is not just for older people. It’s useful for:

- Primary earners: If your family depends on your income, a serious illness could put everyone at risk.

- People with limited savings: If you do not have enough savings to cover at least 6-12 months of living expenses, this insurance can be a safety net.

- People with family history of illness: If close family members had cancer, heart disease, or similar illnesses, your risk may be higher.

- Self-employed or freelancers: Without sick leave or disability coverage, you may need extra protection.

- Parents with young children: To cover child care and education costs if you are unable to work.

Even if you have good health insurance, it may not be enough for the “hidden costs” of a serious illness.

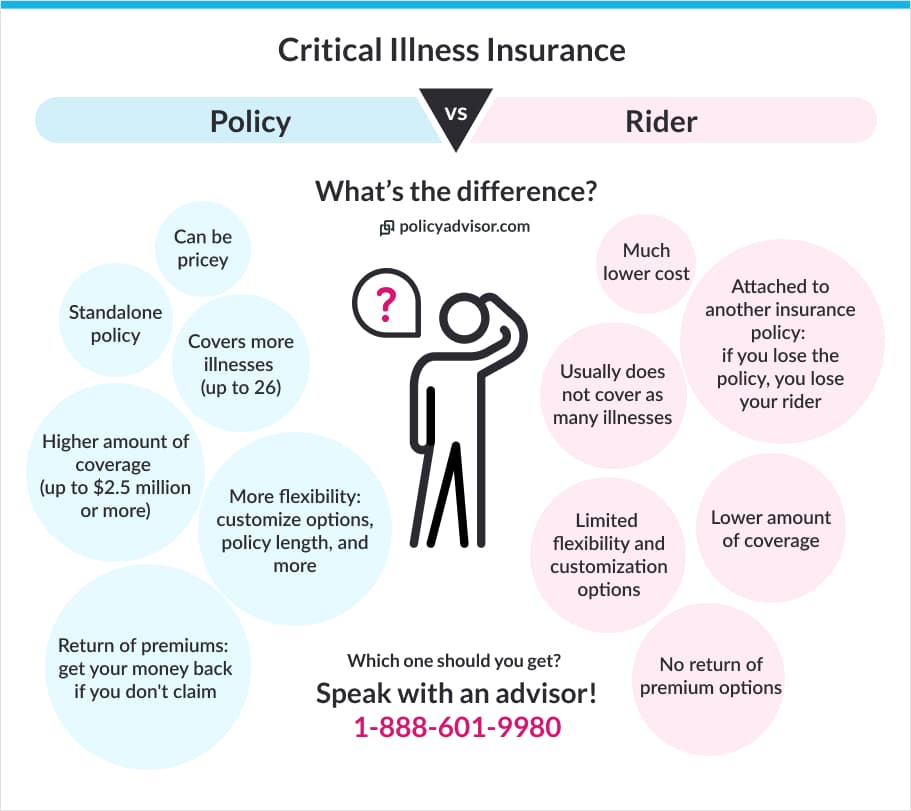

Types Of Critical Illness Insurance Plans

There are two main types:

Standalone Critical Illness Plans

These are separate policies that only pay for covered illnesses. They are simple, with fixed payouts and clear rules.

Rider (add-on) To Life Or Health Insurance

You can add critical illness cover as a “rider” to a life or health policy, often at a lower price. But riders may have lower coverage or more limits.

A quick comparison:

| Type | Coverage | Flexibility | Cost |

|---|---|---|---|

| Standalone Plan | High | More flexible | Higher |

| Rider | Medium | Less flexible | Lower |

Key Factors When Choosing A Plan

Choosing the right critical illness insurance plan is important. Here are some things to check:

- List of covered illnesses: Make sure the diseases that worry you most are included.

- Payout amount: The sum should cover your income for at least 6-12 months, plus extra for medical costs.

- Premium cost: Can you afford the premiums long-term? Cheaper plans may cover fewer illnesses.

- Waiting period: How long must you wait after buying before you can claim?

- Survival period: How long must you survive after diagnosis to receive the benefit?

- Exclusions: Check for hidden rules, like not covering pre-existing conditions, or only paying for severe cases.

- Claim process: Is it easy to file a claim? Are there many documents needed?

Here’s a summary of common plan features:

| Feature | Typical Range |

|---|---|

| Coverage Amount | $10,000 – $500,000 |

| Premium (per year) | $100 – $1,000+ |

| Waiting Period | 30 – 90 days |

| Survival Period | 14 – 30 days |

| Number of Illnesses Covered | 5 – 40+ |

Common Mistakes To Avoid

Many buyers make mistakes when choosing or using critical illness insurance:

- Underestimating coverage needs: Choosing a small sum to save money, but it’s not enough when a crisis happens.

- Ignoring exclusions: Not reading the fine print and discovering some illnesses are not covered.

- Thinking it replaces health insurance: Critical illness cover is for extra protection, not a substitute.

- Letting the policy lapse: Missing payments can mean losing all benefits, even after years of paying.

- Not updating coverage: Life changes—like marriage, kids, or a mortgage—may mean you need more coverage.

Credit: www.policyadvisor.com

Practical Examples

Let’s look at a few real-life examples:

- Case 1: Sarah, 35, buys a $50,000 critical illness policy. At 38, she is diagnosed with breast cancer. Her health insurance covers 80% of hospital bills, but she faces $15,000 in out-of-pocket costs, plus 8 months off work. The critical illness payout helps cover her lost salary and home care.

- Case 2: John, 42, suffers a heart attack. His critical illness plan pays $75,000. He uses some of the money for cardiac rehab and the rest to support his family while he recovers for six months.

- Case 3: Priya, 29, is self-employed. She buys a policy as a rider with her life insurance. After a stroke, she receives $30,000. This covers her rent and therapy, letting her focus on recovery.

These stories show how flexible the payout can be—there are no rules on how you must use the money.

Pros And Cons Of Critical Illness Insurance

Like any insurance, there are good and bad points.

Pros:

- Lump-sum payout can be used for any need

- Covers non-medical costs like living expenses

- Fast payout after a covered illness is diagnosed

- Peace of mind for you and your family

Cons:

- Only covers listed illnesses (not all diseases)

- Premiums can be high for older people or those with health risks

- Strict claim rules—must meet definition of “critical” illness

- May not cover relapse or recurring illnesses

Non-obvious Insights For Buyers

- Many people overlook the survival period rule. Even after diagnosis, if the policyholder does not survive the required period (e.g., 14 days), the payout may not happen.

- Some plans offer partial payouts for early-stage illnesses, but this may reduce the amount available for future claims. Always check if the plan allows multiple claims or only pays once.

- Critical illness cover is often cheaper at a younger age—buying earlier can lock in low rates for years.

- Policies bought through your employer may end if you leave your job—check if you can keep the coverage.

- Some insurers offer wellness programs or discounts for healthy lifestyles, which can save you money.

How To Apply For Critical Illness Insurance

Getting covered is easy, but you must provide:

- Medical history: Past illnesses, surgeries, and current health status

- Family history: Some diseases are more likely if family members had them

- Lifestyle details: Smoking, drinking, and exercise habits

Most insurers require a health check, especially for higher coverage amounts. You must answer truthfully—hiding problems can mean denied claims later.

Alternatives To Critical Illness Insurance

Some people use other ways to protect against big health costs:

- Disability insurance: Replaces a portion of your income if you cannot work due to illness or injury.

- Life insurance: Pays your family if you pass away, but usually does not pay for illness unless you add a rider.

- Health savings accounts (HSAs): Save money tax-free for medical costs.

- Emergency fund: Having 6-12 months of savings gives you flexibility, though not everyone can save this much.

Critical illness insurance offers unique benefits—especially the lump sum and flexibility—making it a useful addition, not a replacement for these other tools.

For more in-depth information, you can visit the NerdWallet Critical Illness Insurance Guide.

Frequently Asked Questions

What Illnesses Are Most Commonly Covered By Critical Illness Insurance?

Most plans cover cancer, heart attack, stroke, kidney failure, and major organ transplant. Some also include multiple sclerosis or paralysis, but always check your policy for the full list.

Is The Payout From Critical Illness Insurance Tax-free?

In the US and many other countries, the lump sum payout is usually tax-free if you paid the premiums yourself. But if your employer paid, there may be taxes—check with a tax advisor.

Can I Buy Critical Illness Insurance If I Already Have Health Issues?

You can apply, but pre-existing conditions are often excluded or may result in higher premiums. Some insurers may decline coverage for certain diseases if you had them before.

How Much Critical Illness Coverage Do I Need?

A good rule is to cover at least 6-12 months of income, plus extra for possible out-of-pocket medical costs. Think about your debts, family needs, and lifestyle.

Can I Have Both Disability And Critical Illness Insurance?

Yes, and many people do. Disability insurance replaces lost income, while critical illness gives a lump sum for any use. Together, they offer stronger protection.

Critical illness insurance can be a lifesaver during one of life’s toughest times. The right plan brings peace of mind, letting you focus on recovery, not bills. Understanding how these policies work—and the details that matter—means you can make a smart choice for yourself and your family.

Credit: www.qian.co.in

Read More:

- Long-Term Disability Insurance Plans: Protect Your Income for Life

- Professional Indemnity Insurance Coverage: Essential Protection Tips

- Cheapest Sr22 Insurance Providers: Top Picks for Budget Drivers

- Landlord Insurance for Rental Properties: Essential Coverage Guide

- Best Life Insurance for Diabetics: Top Plans and Savings Tips

- Best Insurance CRM Software 2026: Top Solutions for Agencies

- Boat Insurance Coverage Options: What You Need to Know

- Car Insurance for Teen Drivers: Save Money and Stay Protected