Professional Indemnity Insurance Coverage: A Complete Guide

Mistakes happen, even to the best professionals. One small error or oversight can lead to big claims and lawsuits. That’s where professional indemnity insurance coverage (often called PI insurance or errors and omissions insurance) steps in. If you’re a consultant, engineer, accountant, designer, or work in any profession where advice or service can cause a client to lose money, understanding this insurance is critical. It protects your career, your finances, and your reputation.

This guide explains what professional indemnity insurance is, what it covers, why it matters, and how to choose the right policy. You’ll also see real-world examples, coverage limits, and common pitfalls to avoid. By the end, you’ll know how to protect yourself and your business from unexpected risks.

What Is Professional Indemnity Insurance Coverage?

Professional indemnity insurance is a special type of business insurance. It protects professionals if a client claims they suffered financial loss because of a mistake, bad advice, or failure to deliver your services as promised. If the client sues, the insurance covers legal defense costs, settlements, and even court-awarded damages.

This coverage is not just for doctors and lawyers. Today, a wide range of professionals need it, including IT consultants, architects, accountants, marketing agencies, and more. In many industries, clients even require you to show proof of PI insurance before hiring you.

Unlike general liability insurance (which covers physical injury or property damage), professional indemnity insurance focuses on financial loss due to your professional services or advice.

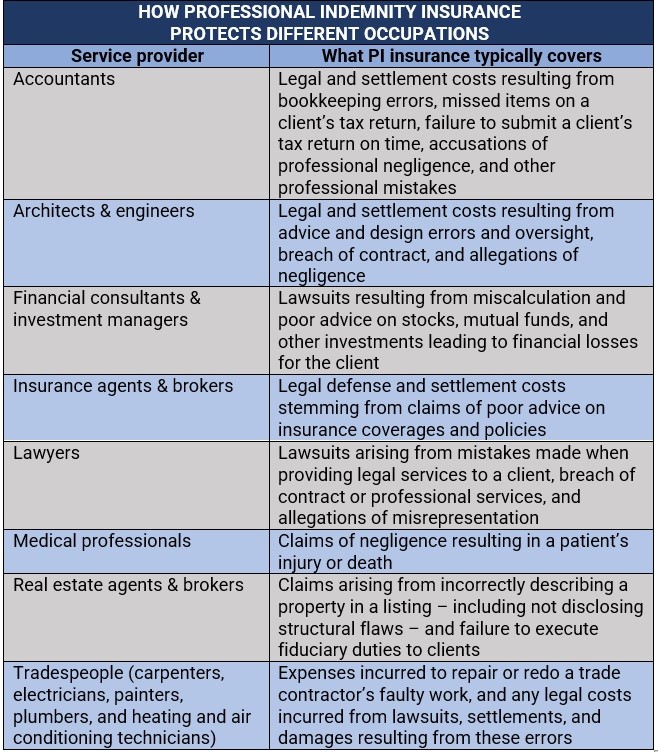

Who Needs Professional Indemnity Insurance?

Not all businesses need PI insurance, but for many, it’s essential. Here are some professions where this coverage is often required or strongly advised:

- Consultants and advisors (business, management, IT, HR)

- Accountants and auditors

- Architects and engineers

- Marketing and advertising agencies

- Designers (graphic, web, interior)

- Lawyers and legal advisors

- Medical professionals (especially for advice, not direct treatment)

- Real estate agents and surveyors

- Technology providers (software developers, IT firms)

- Education and training providers

If your work involves giving advice, making plans, or producing reports that clients rely on, you’re at risk. Even a small error or misunderstanding can lead to a costly claim.

:max_bytes(150000):strip_icc()/Liability-insurance_final-1c2c4bbf923b4933b62582d6d006079c.png)

Credit: www.investopedia.com

What Does Professional Indemnity Insurance Cover?

PI insurance covers a wide range of risks related to your professional services. Here’s what’s typically included:

- Negligence: Errors, omissions, or mistakes in your work that cause a client financial loss.

- Breach of duty: Failing to meet industry standards or contractual obligations.

- Defamation: Claims that you made false or damaging statements about a client or third party.

- Loss of documents/data: Accidentally losing client documents or data, whether physical or digital.

- Intellectual property infringement: Accidentally using someone else’s copyrighted material, design, or trademark.

- Unintentional breach of confidentiality: Accidentally sharing a client’s confidential information.

- Legal costs: Paying for lawyers, court fees, and settlements—even if the claim is groundless.

Real-world Example

A management consultant gives advice that leads to a client losing $100,000 in revenue. The client blames the consultant and sues for damages. The consultant’s PI insurance covers legal fees and, if needed, any settlement.

What’s Not Covered

PI insurance doesn’t cover everything. Common exclusions include:

- Intentional wrongdoing or criminal acts

- Bodily injury or property damage (use general liability insurance)

- Employee claims (use workers’ compensation)

- Known claims before the policy started

- Fines and penalties from regulatory bodies

It’s important to read your policy carefully and ask questions.

How Does Professional Indemnity Insurance Work?

PI insurance works on a “claims-made” basis. This means your policy must be active both when the incident happens and when the claim is made. If you cancel your policy or let it lapse, you may not be covered—even for things that happened when you were insured.

Claims-made Example

- You give advice to a client in 2023.

- In 2024, the client discovers a problem and files a claim.

- Your policy must be active in 2024 (when the claim is made) to cover the loss.

Tip: Always keep your PI insurance active while you’re in business and for several years after you stop (this is called “run-off” coverage).

Credit: www.insurancebusinessmag.com

How Much Coverage Do You Need?

Choosing the right coverage limit is one of the most important decisions. Too little, and you risk paying big costs yourself. Too much, and you may pay more than necessary.

Factors To Consider

- Contract requirements: Clients often set a minimum coverage amount.

- Size of projects: Larger projects and high-value clients mean higher risks.

- Industry standards: Some professions have typical coverage amounts.

- Legal environment: Lawsuits are more common (and expensive) in some industries or countries.

Typical Coverage Limits

Coverage amounts can range widely, often from $250,000 to $5 million or more. Here’s a quick look:

| Profession | Common Coverage Limit |

|---|---|

| Small Consultant | $250,000 – $1 million |

| Architect/Engineer | $1 million – $5 million |

| Large IT Firm | $2 million – $10 million |

| Law Firm | $1 million – $10 million |

Insight: Most claims are under $100,000, but rare cases can exceed $1 million. Check your industry’s risk profile.

Common Claims And Real-world Scenarios

Understanding what real claims look like can help you assess your risk. Here are a few examples:

- IT consultant: Accidentally deletes client data during a software upgrade. The client sues for the cost of lost business.

- Architect: Makes a design error, leading to construction delays and extra costs. The client files a claim for damages.

- Accountant: Mistakenly files incorrect tax returns, causing the client to pay penalties and back taxes.

- Marketing agency: Uses an image without proper license, and the copyright owner sues for infringement.

Non-obvious insight: Even if you win in court, defense costs can be high. PI insurance pays for legal defense, which can sometimes exceed the value of the claim itself.

What Impacts The Cost Of Pi Insurance?

PI insurance premiums depend on your business risk profile. Key factors include:

- Type of profession: Higher-risk industries pay more.

- Business size and revenue: More clients and higher revenue mean more exposure.

- Claims history: Past claims can raise premiums.

- Coverage amount: Higher limits cost more.

- Location: Some regions have more lawsuits or higher legal costs.

Here’s a comparison of average annual PI insurance costs:

| Profession | Estimated Annual Premium |

|---|---|

| Freelance Designer | $400 – $800 |

| IT Consultant | $600 – $1,500 |

| Architect | $1,200 – $3,500 |

| Accountant | $900 – $2,000 |

Tip: Premiums can be negotiated. If you have a good claims record, ask for a discount.

How To Choose The Right Policy

Selecting the right PI insurance isn’t just about the price. Here’s what matters:

- Insurer’s reputation: Choose a company with a strong claims history and financial stability.

- Policy wording: Make sure all your services are covered. Ask for examples and definitions.

- Coverage limits and deductibles: Balance premium cost with the amount you can afford to pay if there’s a claim.

- Retroactive cover: Some insurers offer coverage for past work. Check if this is included.

- Exclusions: Read the fine print. Some policies exclude certain activities or types of claims.

- Claims process: Ask how claims are handled and how quickly the insurer responds.

Common Mistakes When Buying Pi Insurance

- Underestimating risks: Choosing the minimum required by a client may not be enough for your real exposure.

- Ignoring retroactive cover: If you switch insurers, make sure your new policy covers past work.

- Not updating the policy: As your business grows or changes, update your coverage.

- Assuming all activities are covered: Some policies exclude new services unless you inform the insurer.

Non-obvious tip: Insurers sometimes deny claims for late notification. Always report incidents or potential claims as soon as possible—even if you think it’s a small issue.

Pi Insurance Vs. Other Business Insurance

Many business owners confuse PI insurance with other types of coverage. Here’s a simple comparison:

| Insurance Type | Main Focus | Example Claim |

|---|---|---|

| Professional Indemnity | Financial loss from professional errors | Bad advice causes client loss |

| General Liability | Bodily injury, property damage | Client slips and falls in your office |

| Directors & Officers | Claims against company directors | Shareholders sue for mismanagement |

| Cyber Liability | Data breaches, cyberattacks | Hackers steal client data |

Insight: Most professional firms need at least PI and general liability insurance. Some industries also need cyber or D&O insurance.

How To File A Claim

If a client threatens legal action or complains about your work, act fast:

- Notify your insurer immediately—even if you’re not sure it’s a real claim.

- Collect all documents: Contracts, emails, reports, and anything related to the project.

- Do not admit liability: Let your insurer handle communication with the client.

- Work with the insurer’s legal team: They’ll help defend your case or negotiate a settlement.

Delays or mistakes in the process can lead to denied claims. Quick action is your best protection.

Credit: www.insurancebusinessmag.com

Real Benefits Beyond Financial Protection

PI insurance is more than just a safety net. Here’s what it can do for your business:

- Win more clients: Many organizations require proof of PI insurance before signing a contract.

- Peace of mind: You can focus on your work, knowing you’re protected from costly mistakes.

- Better professional image: Having insurance shows clients you’re responsible and trustworthy.

- Access to legal experts: Insurers often provide specialist lawyers who know your industry.

Practical insight: Some professional bodies make PI insurance mandatory for membership. Check your industry’s rules.

Frequently Asked Questions

What Is The Difference Between Professional Indemnity And General Liability Insurance?

Professional indemnity insurance covers financial losses caused by professional mistakes, bad advice, or negligence. General liability insurance covers physical injury or property damage. For example, if your advice leads to a client losing money, PI covers it. If a client slips in your office, general liability covers it.

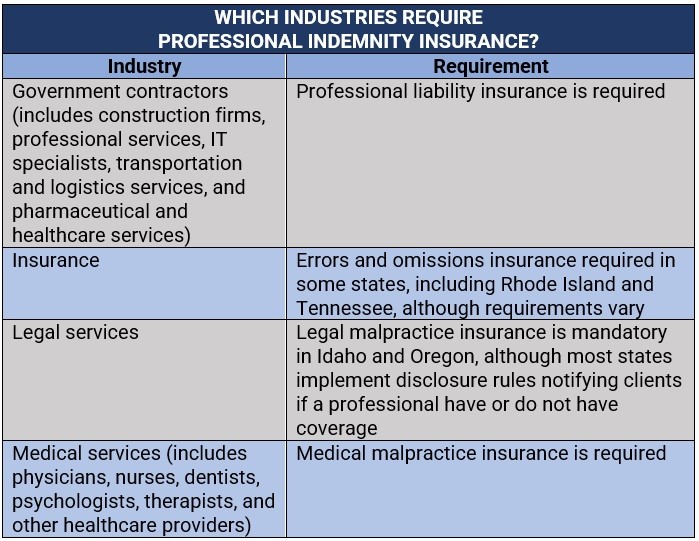

Is Professional Indemnity Insurance Mandatory?

In some industries and countries, PI insurance is mandatory by law or by professional bodies. Even if it’s not required, many clients demand it in contracts. It’s best to check both legal requirements and client expectations before starting work.

How Much Does Professional Indemnity Insurance Cost?

Costs depend on your profession, business size, claims history, and coverage limits. Freelancers may pay a few hundred dollars a year, while large firms may pay thousands. Get quotes from several insurers and compare coverage, not just price.

How Long Should I Keep Pi Insurance?

Keep your PI insurance active as long as you provide professional services. Consider “run-off” cover for several years after you retire or close your business, because claims can be made long after the work was done.

Where Can I Learn More About Professional Indemnity Insurance?

For more detailed information, visit the Wikipedia page on professional liability insurance. It covers industry standards, legal aspects, and international differences.

Professional indemnity insurance coverage is an essential tool for protecting your reputation, finances, and career. By choosing the right policy and understanding how it works, you can safeguard your business from costly mistakes and focus on growing your success. Don’t wait for a claim to learn the hard way—get covered and stay protected.

Read More:

- Critical Illness Insurance Plans: Protect Your Future Today

- Long-Term Disability Insurance Plans: Protect Your Income for Life

- Cheapest Sr22 Insurance Providers: Top Picks for Budget Drivers

- Landlord Insurance for Rental Properties: Essential Coverage Guide

- Best Life Insurance for Diabetics: Top Plans and Savings Tips

- Best Insurance CRM Software 2026: Top Solutions for Agencies

- Boat Insurance Coverage Options: What You Need to Know

- Car Insurance for Teen Drivers: Save Money and Stay Protected