Millions of people in the United States rely on private health insurance to protect themselves from high medical costs. But the process of finding, comparing, and buying a plan can feel confusing, especially if you are new to the private health insurance marketplace. Understanding how this marketplace works, what choices you have, and what mistakes to avoid is important if you want good coverage without paying too much. This article explains the basics of private health insurance marketplaces, compares plans, shares useful tips, and answers common questions—all in clear, simple language.

What Is The Private Health Insurance Marketplace?

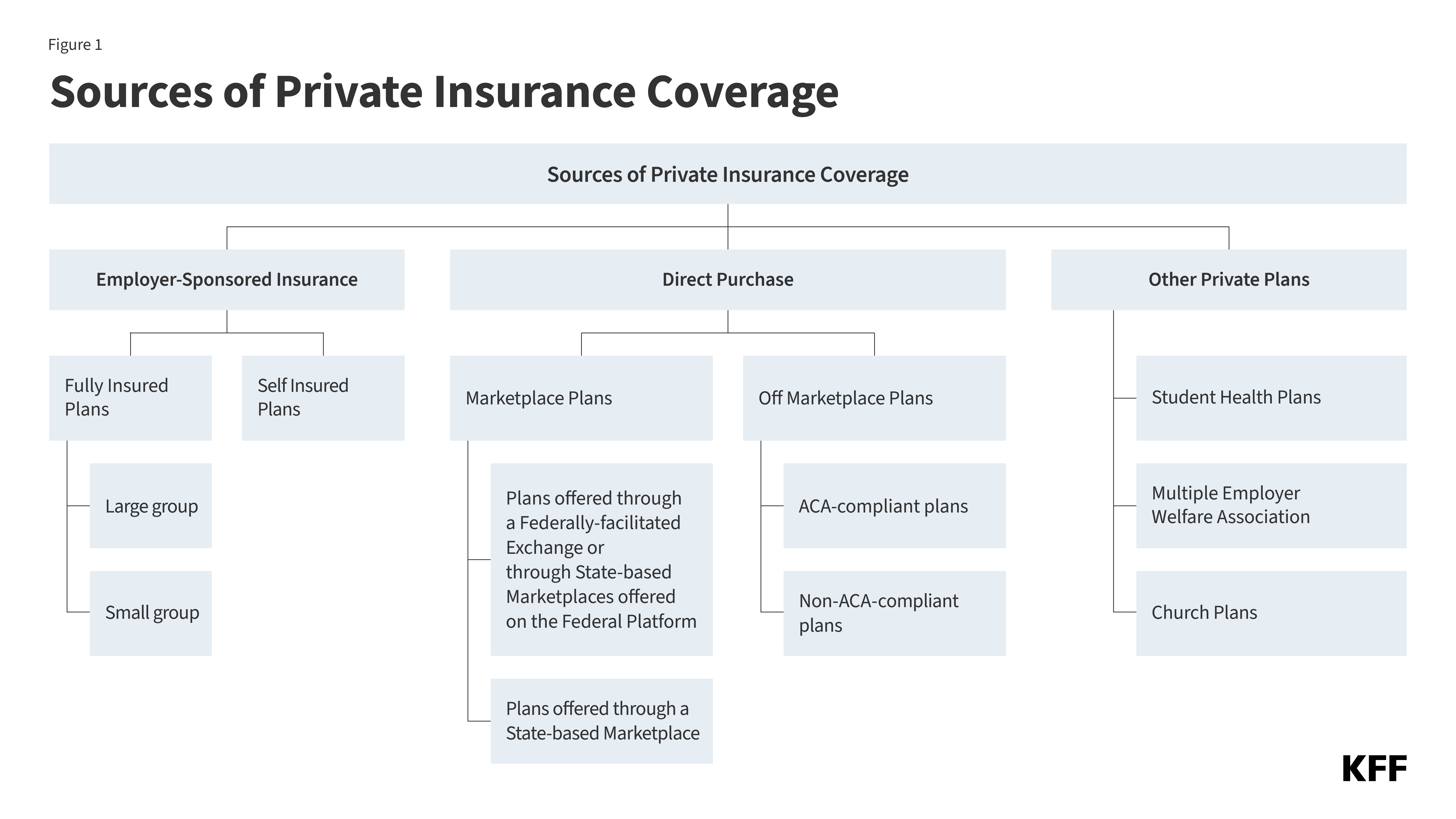

The private health insurance marketplace is where individuals and families buy health insurance directly from private companies. Unlike government programs like Medicare or Medicaid, private insurance is paid for by the consumer or their employer. There are two main ways to access the marketplace:

- Employer-sponsored plans: Many Americans get coverage through their employer. Employers usually offer several plan options, and pay part of the monthly premium.

- Individual and family plans: People who do not have employer coverage can buy insurance directly from private companies or through brokers.

You can find plans on company websites, through licensed agents, or using online comparison platforms. These platforms help you compare costs, benefits, and provider networks.

How Private Health Insurance Differs From Public Insurance

Private health insurance is not the same as public options like Medicare or Medicaid. Here are some key differences:

- Eligibility: Private insurance is open to anyone who can pay for it; public programs have strict eligibility rules.

- Coverage: Private plans often offer more choices, but you must pay premiums, deductibles, and copayments.

- Flexibility: You can select the plan that fits your needs and budget. Public insurance usually gives less choice.

Some people have both types—for example, Medicare plus a private plan—to cover gaps.

Types Of Private Health Insurance Plans

Choosing the right plan is easier when you understand the main types. Here’s a quick overview:

| Plan Type | How It Works | Typical Cost | Network Flexibility |

|---|---|---|---|

| HMO (Health Maintenance Organization) | Must use network doctors; need referral for specialists | Lower premiums | Limited; must stay in network |

| PPO (Preferred Provider Organization) | Can see any doctor; no referral needed | Higher premiums | Flexible; both in- and out-of-network |

| EPO (Exclusive Provider Organization) | Must use network doctors; no referrals needed | Medium premiums | Limited; only in network |

| POS (Point of Service) | Mix of HMO and PPO; referrals needed for out-of-network | Medium premiums | Some flexibility |

Most people choose between HMO and PPO. HMOs are cheaper but strict; PPOs cost more but offer freedom. If you travel often or want to see specialists without waiting, PPO may be better.

Comparing Costs: Premiums, Deductibles, And Out-of-pocket

Understanding health insurance costs is key. Here are the main terms:

- Premium: The monthly fee you pay for insurance.

- Deductible: The amount you must pay before insurance starts covering costs.

- Copayment: A fixed fee for each doctor visit or prescription.

- Out-of-pocket maximum: The most you will pay in one year, after which insurance pays all covered costs.

Here’s a simple comparison of typical costs for individual plans:

| Plan Type | Monthly Premium | Deductible | Out-of-Pocket Max |

|---|---|---|---|

| HMO | $350 | $2,000 | $7,500 |

| PPO | $450 | $1,000 | $6,500 |

| EPO | $400 | $1,500 | $7,000 |

| POS | $425 | $1,200 | $6,800 |

Prices change by age, state, and plan level. Younger people pay less, older people pay more. Families pay higher premiums than individuals.

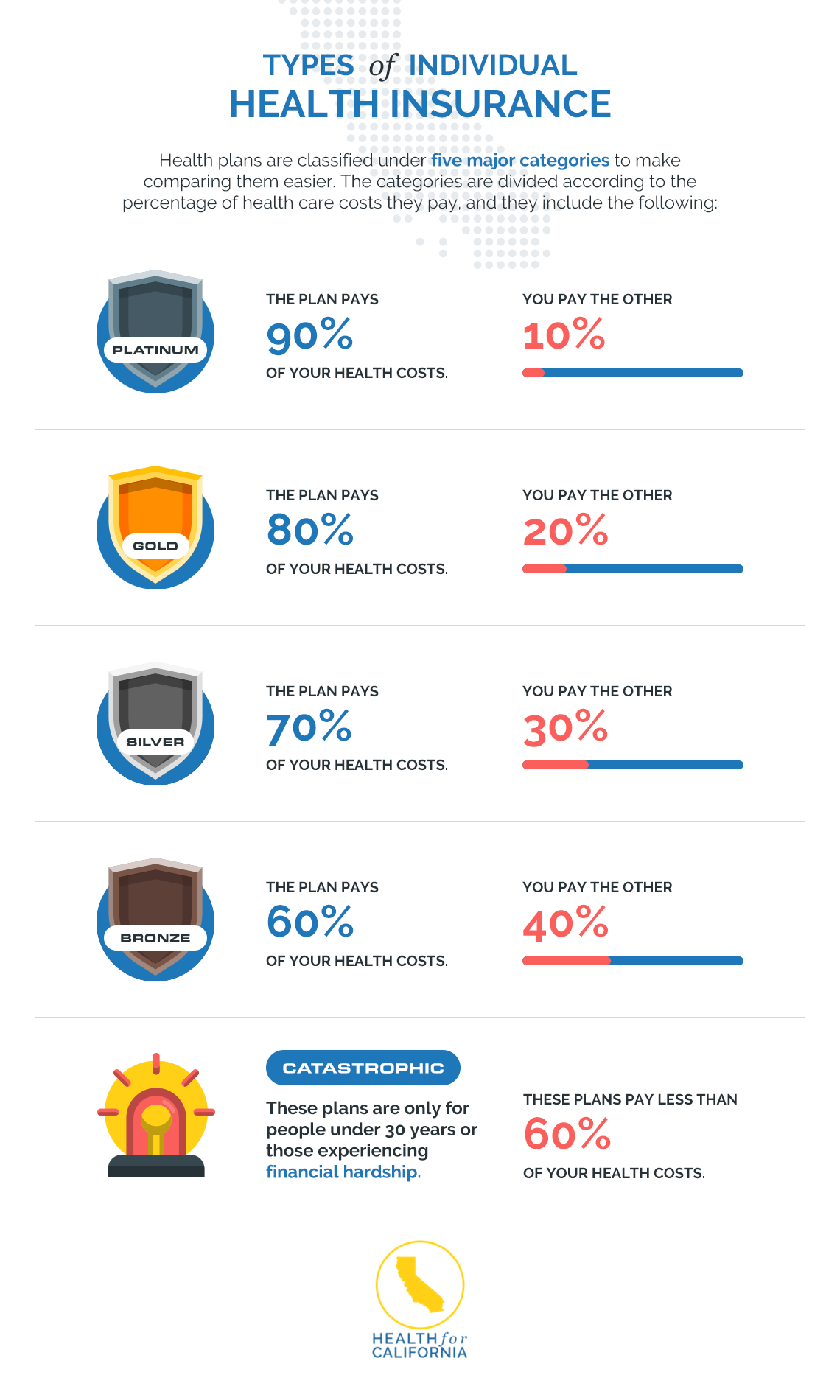

Credit: www.healthforcalifornia.com

What To Look For When Choosing A Plan

Choosing a plan is not just about price. Consider these important factors:

- Coverage: Make sure the plan covers your needs. Check if doctors, hospitals, and medicines are included.

- Network: Are your preferred doctors and hospitals in the network? Out-of-network care costs much more.

- Costs: Look beyond the premium. High deductibles or copayments can mean bigger bills.

- Extras: Some plans offer dental, vision, or wellness benefits.

- Customer service: Good support matters when you need help or have claims.

A common mistake is picking the cheapest plan without checking coverage. Cheap plans can lead to big bills if you get sick or injured.

How The Marketplace Works: Buying And Enrollment

The private health insurance marketplace is busiest during Open Enrollment. This is a set period each year when you can sign up, change, or cancel coverage. Outside this window, you need a qualifying event (like marriage, birth, job loss) to enroll.

Steps to buy a plan:

- Research: Use comparison websites, company platforms, or brokers to see your options.

- Compare: Look at premiums, deductibles, networks, and extras.

- Apply: Fill out an online application. You may need to answer health questions.

- Pay: Once approved, pay the first premium to activate your coverage.

- Receive ID: You’ll get an insurance card and policy documents.

Many platforms now offer online tools to help you estimate costs, compare plans, and check if your doctor is in-network.

Credit: stateline.org

Regulatory Changes And The Affordable Care Act

In 2010, the Affordable Care Act (ACA) changed the private health insurance landscape. The ACA made coverage easier to get and more affordable for many people. Key changes include:

- No denial for pre-existing conditions

- Coverage for essential health benefits

- Subsidies for low-income buyers

Private insurance companies must follow ACA rules, but they still set prices and coverage details. Some states run their own marketplaces; others use the federal platform.

Common Mistakes In The Marketplace

New buyers often make these mistakes:

- Ignoring the network: Not checking if your doctor is covered can lead to surprise bills.

- Underestimating deductibles: Low premiums often come with high deductibles.

- Missing enrollment deadlines: If you miss Open Enrollment, you may have to wait a year.

- Skipping extras: Dental and vision are often not included; check before buying.

A non-obvious mistake is forgetting about prescription drug coverage. Some plans do not cover all medicines, so check the formulary list.

Credit: www.kff.org

Non-obvious Insights For Beginners

- Check hospital coverage: Plans may list a hospital as “in-network” but only cover certain services. Ask for details before buying.

- Know your annual limits: Some plans cap the amount paid for certain treatments. If you have ongoing health issues, check these limits.

- Watch for renewal rules: Private plans may change terms each year. Always read renewal notices to avoid surprise changes.

- Understand telemedicine benefits: Many plans now cover virtual visits, which can save time and money.

These details can save you from unexpected costs or gaps in coverage.

How To Save Money In The Private Marketplace

Health insurance is expensive, but you can reduce costs:

- Shop around: Compare at least three plans before buying.

- Use preventive care: Many plans cover checkups for free. Staying healthy lowers long-term costs.

- Ask about subsidies: If your income is low, you may qualify for ACA subsidies.

- Choose a higher deductible: If you rarely need care, a higher deductible plan can lower your premium.

- Bundle coverage: Some companies offer discounts for adding dental or vision.

For more money-saving tips and resources, visit the official Healthcare.gov site.

Trends And Future Of Private Health Insurance Marketplace

The marketplace is changing fast. Here are some trends:

- Telemedicine: More plans cover online doctor visits.

- Personalized plans: Companies use data to offer plans tailored to your health needs.

- Digital tools: Online platforms make comparing and buying easier.

- Wellness incentives: Some plans reward healthy behaviors with lower costs.

Statistics show that in 2023, over 16 million Americans bought private insurance through ACA marketplaces, and millions more used employer-sponsored plans.

Real-life Example

Emily, a 32-year-old freelancer, needed private insurance. She compared HMO and PPO plans online. The HMO was cheaper but did not include her preferred hospital. The PPO cost more but covered her doctors and offered telemedicine. Emily chose the PPO for flexibility.

Later, she used telemedicine for a quick issue, saving both time and money.

Frequently Asked Questions

What Is The Difference Between Private And Public Health Insurance?

Private health insurance is sold by companies and is open to most people. Public insurance like Medicare and Medicaid is run by the government and has strict eligibility rules. Private insurance offers more plan choices, but you pay premiums and costs.

How Can I Find The Best Plan For My Needs?

Start by listing your health needs—do you see specialists, need regular medicines, or want certain hospitals? Use comparison platforms to check coverage, costs, and networks. Ask questions before buying. Look for online reviews and customer ratings.

Are Pre-existing Conditions Covered In Private Plans?

Yes, since the Affordable Care Act, private plans cannot deny coverage for pre-existing conditions. But some older or short-term plans may have limits, so always check the policy details.

Can I Get Subsidies To Lower My Premiums?

If your income is low or moderate, you may qualify for subsidies through ACA marketplaces. These can reduce your monthly premium and out-of-pocket costs. Check eligibility at Healthcare. gov or your state marketplace.

What Happens If I Miss Open Enrollment?

If you miss Open Enrollment, you cannot buy or change your plan until the next period, unless you have a qualifying event like marriage, birth, or job loss. Some short-term plans are available, but they may not cover as much.

Private health insurance marketplaces give you freedom and protection but require careful choices. Use the tips and comparisons in this article to find the best plan for your needs and budget. Remember, a smart decision today can mean peace of mind and savings tomorrow.

Read More:

- Critical Illness Insurance Plans: Protect Your Future Today

- Long-Term Disability Insurance Plans: Protect Your Income for Life

- Professional Indemnity Insurance Coverage: Essential Protection Tips

- Cheapest Sr22 Insurance Providers: Top Picks for Budget Drivers

- Landlord Insurance for Rental Properties: Essential Coverage Guide

- Best Life Insurance for Diabetics: Top Plans and Savings Tips

- Best Insurance CRM Software 2026: Top Solutions for Agencies

- Boat Insurance Coverage Options: What You Need to Know